In the intricate world of corporate finance, few phrases evoke as much dread as “bad debt expense․” It signifies a loss, a recognition that money once anticipated will likely never materialize․ For countless businesses, from burgeoning startups to established multinational corporations, bad debt is often viewed as an inevitable, albeit painful, cost of doing business – a write-off simply absorbed and moved past․ Yet, what if this widely accepted narrative overlooks a powerful, incredibly effective strategy for financial recovery? What if there’s a largely untapped mechanism that allows companies to not just mitigate but actively credit bad debt expense, transforming past losses into future gains and fundamentally reshaping their financial outlook?

Indeed, the idea of crediting bad debt expense might initially sound counterintuitive, even heretical, to those steeped in traditional accounting principles․ After all, expenses are typically debited, reflecting a reduction in equity․ However, a deeper dive into the sophisticated mechanics of modern accounting, particularly concerning the recovery of previously written-off accounts, reveals a remarkably optimistic truth․ This isn’t just about minimizing future losses; it’s about strategically reclaiming historical ones, thereby bolstering profitability, enhancing cash flow, and providing a compelling testament to robust financial management․ Savvy finance professionals are increasingly leveraging these often-misunderstood procedures to unlock hidden value, proving that yesterday’s liabilities can astonishingly become today’s assets․

| Aspect | Description | Accounting Impact (Recovery Scenario) |

|---|---|---|

| Bad Debt Expense | An estimate of uncollectible accounts receivable, recognized in the period the related sale occurred, reducing net income․ | Initially a debit (expense) to reflect expected losses․ A recovery of a previously written-off debt can lead to a credit (reduction) to Bad Debt Expense or the Allowance for Doubtful Accounts, effectively boosting net income․ |

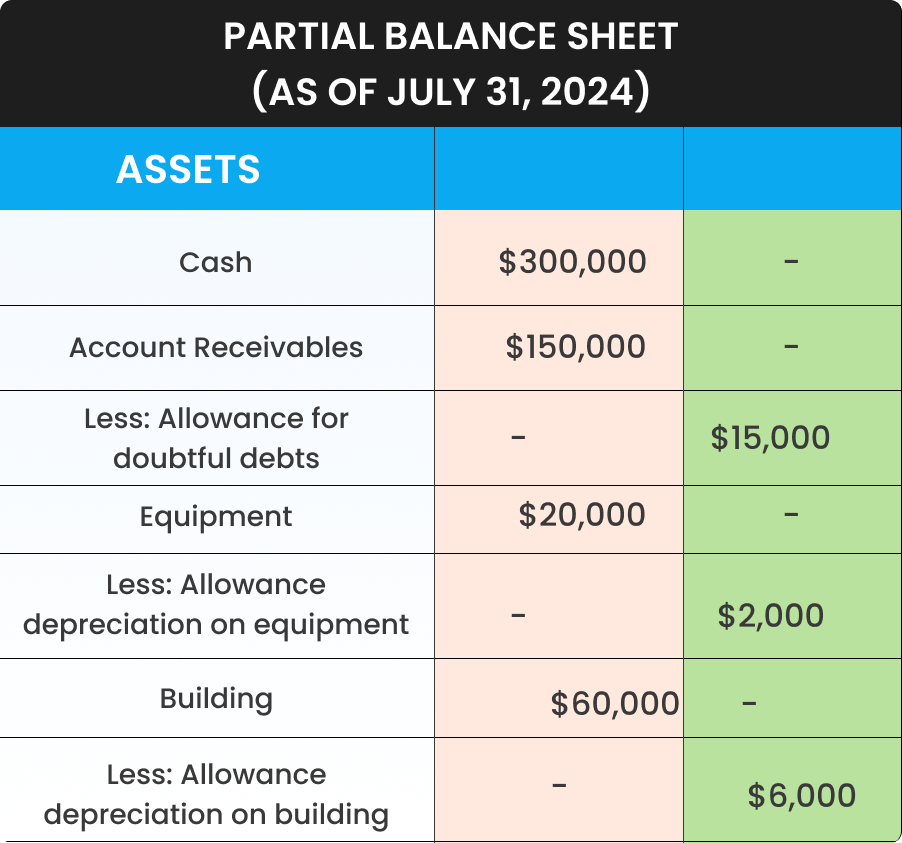

| Allowance for Doubtful Accounts | A contra-asset account, reducing the gross amount of Accounts Receivable to its estimated net realizable value on the balance sheet․ | Typically credited when bad debt expense is recognized․ Debited when a specific account is deemed uncollectible and formally written off․ Crucially, it is credited again upon recovery, reinstating the receivable․ |

| Accounts Receivable Write-off | The formal removal of a specific uncollectible customer account from the company’s active ledger, often after extensive collection efforts fail․ | Debits Allowance for Doubtful Accounts and Credits Accounts Receivable․ This action typically has no direct impact on Bad Debt Expense at the time of write-off if the allowance method is being utilized․ |

| Recovery of Written-Off Debt | The unexpected event where a customer pays an amount that was previously considered uncollectible and formally removed from the books․ | This involves a two-step accounting process:

The net effect is a reduction in the overall bad debt expense for the period, improving financial metrics․ |

| GAAP/IFRS Treatment | Both Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) mandate the use of the allowance method for estimating and recognizing bad debts, ensuring expenses are matched to revenues․ | Accounting for recoveries is consistent across both frameworks: reinstate the receivable and then record the cash․ This systematic approach ensures financial statements accurately reflect the true economic substance of these transactions․ |

The Alchemy of Recovery: Transforming Losses into Ledger Gains

Understanding how to effectively credit bad debt expense lies at the heart of sophisticated financial stewardship․ When a company determines that a specific account receivable is uncollectible, it typically utilizes the allowance method, debiting Bad Debt Expense and crediting Allowance for Doubtful Accounts․ This approach adheres to the matching principle, ensuring that the expense is recognized in the same period as the related revenue․ However, the story doesn’t always end there․ Imagine a scenario where, months or even years after an account has been written off, the previously delinquent customer surprisingly remits payment․ This isn’t just a happy accident; it’s a critical moment for financial re-evaluation․

According to esteemed accounting expert Dr․ Alistair Finch, a professor of financial reporting at the London School of Economics, “The recovery of a written-off debt isn’t merely found money; it’s a testament to the dynamic nature of financial health․ Proper accounting treatment for such recoveries involves reversing the original write-off, thereby reinstating the receivable, and then recording the cash receipt․ This sequence effectively credits the Allowance for Doubtful Accounts, which in turn reduces the cumulative bad debt expense for the period․” This meticulous process, while seemingly complex, directly impacts a company’s bottom line, translating what was once a definitive loss into a tangible gain․ It underscores the profound importance of maintaining diligent records and actively pursuing even dormant receivables․

Industry Insights: Where Recovery Shines Brightest

The strategic crediting of bad debt expense through recoveries holds particular significance in industries characterized by high volumes of accounts receivable and fluctuating customer solvency․ Consider the healthcare sector, where patient balances can become complex and collections arduous․ Hospitals and clinics, often burdened by extensive write-offs, can significantly benefit from robust systems designed to track and recover these debts, improving their operational margins dramatically․ Similarly, in retail and financial services, where credit lines and installment plans are commonplace, the ability to reclaim previously written-off balances directly enhances profitability and reinforces the efficacy of their credit risk models․

For instance, a major telecommunications provider, having written off thousands of small, uncollectible balances during an economic downturn, might later engage a specialized recovery agency․ Should these efforts prove successful, the subsequent influx of cash, meticulously accounted for as a recovery, directly lessens the impact of past bad debt provisions․ This isn’t just about cash injection; it’s about validating the long-term potential of customer relationships and demonstrating a proactive stance towards financial integrity, painting a much brighter picture for stakeholders and investors alike․

The Future of Financial Foresight: Leveraging Technology for Unprecedented Recovery

Looking ahead, the landscape of bad debt management is evolving at an astonishing pace, driven by advancements in data analytics and artificial intelligence․ Companies are no longer content with reactive measures; instead, they are proactively employing sophisticated algorithms to predict payment behaviors, identify high-recovery potential accounts, and optimize collection strategies․ By integrating insights from AI-driven predictive models, businesses can not only minimize initial bad debt provisions but also significantly enhance their chances of recovering previously written-off amounts․

This forward-looking approach transforms bad debt from a static liability into a dynamic opportunity for financial optimization․ Imagine AI algorithms sifting through vast datasets, identifying specific customer segments that, despite past defaults, now exhibit indicators of improved financial stability․ This intelligence allows companies to target recovery efforts with unparalleled precision, turning what was once a laborious and often fruitless endeavor into an incredibly effective, data-backed strategy․ The future isn’t just about reducing bad debt; it’s about mastering its lifecycle, crediting those expenses when opportunities arise, and ultimately, building more resilient and profitable enterprises․